Williams-Sonoma, Inc. (NYSE:WSM): 3 Days To Buy Before The Ex-Dividend Date

On the 22 February 2019, Williams-Sonoma, Inc. (NYSE:WSM) will be paying shareholders an upcoming dividend amount of US$0.43 per share. However, investors must have bought the company’s stock before 24 January 2019 in order to qualify for the payment. That means you have only 3 days left! Should you diversify into Williams-Sonoma and boost your portfolio income stream? Well, keep on reading because today, I’m going to look at the latest data and analyze the stock and its dividend property in further detail.

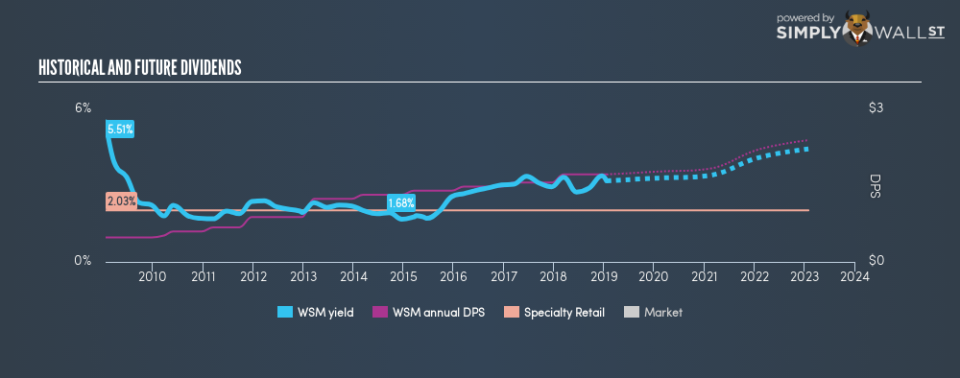

Check out our latest analysis for Williams-Sonoma

Want to help shape the future of investing tools and platforms? Take the survey and be part of one of the most advanced studies of stock market investors to date.

5 questions I ask before picking a dividend stock

When researching a dividend stock, I always follow the following screening criteria:

Is it paying an annual yield above 75% of dividend payers?

Has its dividend been stable over the past (i.e. no missed payments or significant payout cuts)?

Has it increased its dividend per share amount over the past?

Does earnings amply cover its dividend payments?

Based on future earnings growth, will it be able to continue to payout dividend at the current rate?

Does Williams-Sonoma pass our checks?

The current trailing twelve-month payout ratio for the stock is 51%, meaning the dividend is sufficiently covered by earnings. In the near future, analysts are predicting lower payout ratio of 42% which, assuming the share price stays the same, leads to a dividend yield of around 3.4%. However, EPS should increase to $4.34, meaning that the lower payout ratio does not necessarily implicate a lower dividend payment.

If you want to dive deeper into the sustainability of a certain payout ratio, you may wish to consider the cash flow of the business. Companies with strong cash flow can sustain a higher payout ratio, while companies with weaker cash flow generally cannot.

If there’s one type of stock you want to be reliable, it’s dividend stocks and their stable income-generating ability. WSM has increased its DPS from $0.48 to $1.72 in the past 10 years. It has also been paying out dividend consistently during this time, as you’d expect for a company increasing its dividend levels. These are all positive signs of a great, reliable dividend stock.

In terms of its peers, Williams-Sonoma produces a yield of 3.2%, which is high for Specialty Retail stocks but still below the market’s top dividend payers.

Next Steps:

With this in mind, I definitely rank Williams-Sonoma as a strong dividend stock, and makes it worth further research for anyone who likes steady income generation from their portfolio. Given that this is purely a dividend analysis, I urge potential investors to try and get a good understanding of the underlying business and its fundamentals before deciding on an investment. Below, I’ve compiled three key aspects you should further research:

Future Outlook: What are well-informed industry analysts predicting for WSM’s future growth? Take a look at our free research report of analyst consensus for WSM’s outlook.

Valuation: What is WSM worth today? Even if the stock is a cash cow, it’s not worth an infinite price. The intrinsic value infographic in our free research report helps visualize whether WSM is currently mispriced by the market.

Other Dividend Rockstars: Are there better dividend payers with stronger fundamentals out there? Check out our free list of these great stocks here.

To help readers see past the short term volatility of the financial market, we aim to bring you a long-term focused research analysis purely driven by fundamental data. Note that our analysis does not factor in the latest price-sensitive company announcements.

The author is an independent contributor and at the time of publication had no position in the stocks mentioned. For errors that warrant correction please contact the editor at editorial-team@simplywallst.com.