Should We Worry About Northwest Pipe Company's (NASDAQ:NWPX) P/E Ratio?

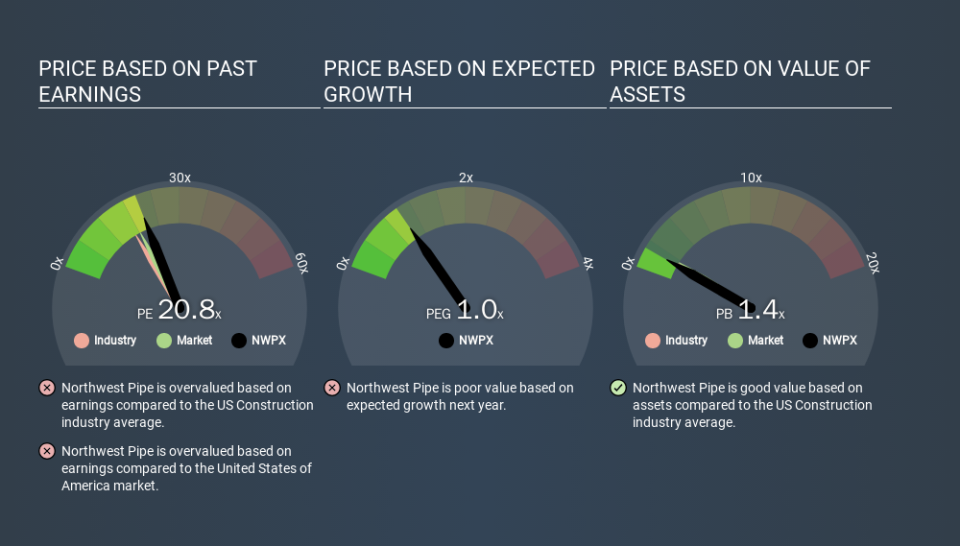

The goal of this article is to teach you how to use price to earnings ratios (P/E ratios). We'll look at Northwest Pipe Company's (NASDAQ:NWPX) P/E ratio and reflect on what it tells us about the company's share price. Northwest Pipe has a price to earnings ratio of 20.81, based on the last twelve months. That means that at current prices, buyers pay $20.81 for every $1 in trailing yearly profits.

See our latest analysis for Northwest Pipe

How Do I Calculate A Price To Earnings Ratio?

The formula for price to earnings is:

Price to Earnings Ratio = Share Price ÷ Earnings per Share (EPS)

Or for Northwest Pipe:

P/E of 20.81 = $34.27 ÷ $1.65 (Based on the year to September 2019.)

Is A High Price-to-Earnings Ratio Good?

A higher P/E ratio means that investors are paying a higher price for each $1 of company earnings. That is not a good or a bad thing per se, but a high P/E does imply buyers are optimistic about the future.

Does Northwest Pipe Have A Relatively High Or Low P/E For Its Industry?

We can get an indication of market expectations by looking at the P/E ratio. As you can see below, Northwest Pipe has a higher P/E than the average company (16.9) in the construction industry.

Its relatively high P/E ratio indicates that Northwest Pipe shareholders think it will perform better than other companies in its industry classification. The market is optimistic about the future, but that doesn't guarantee future growth. So investors should always consider the P/E ratio alongside other factors, such as whether company directors have been buying shares.

How Growth Rates Impact P/E Ratios

Earnings growth rates have a big influence on P/E ratios. That's because companies that grow earnings per share quickly will rapidly increase the 'E' in the equation. And in that case, the P/E ratio itself will drop rather quickly. A lower P/E should indicate the stock is cheap relative to others -- and that may attract buyers.

Northwest Pipe shrunk earnings per share by 13% over the last year. But it has grown its earnings per share by 8.8% per year over the last five years.

Don't Forget: The P/E Does Not Account For Debt or Bank Deposits

The 'Price' in P/E reflects the market capitalization of the company. So it won't reflect the advantage of cash, or disadvantage of debt. Theoretically, a business can improve its earnings (and produce a lower P/E in the future) by investing in growth. That means taking on debt (or spending its cash).

Such spending might be good or bad, overall, but the key point here is that you need to look at debt to understand the P/E ratio in context.

Northwest Pipe's Balance Sheet

The extra options and safety that comes with Northwest Pipe's US$12m net cash position means that it deserves a higher P/E than it would if it had a lot of net debt.

The Verdict On Northwest Pipe's P/E Ratio

Northwest Pipe's P/E is 20.8 which is above average (18.3) in its market. The recent drop in earnings per share would make some investors cautious, but the relatively strong balance sheet will allow the company time to invest in growth. Clearly, the high P/E indicates shareholders think it will!

Investors have an opportunity when market expectations about a stock are wrong. As value investor Benjamin Graham famously said, 'In the short run, the market is a voting machine but in the long run, it is a weighing machine. So this free visual report on analyst forecasts could hold the key to an excellent investment decision.

You might be able to find a better buy than Northwest Pipe. If you want a selection of possible winners, check out this free list of interesting companies that trade on a P/E below 20 (but have proven they can grow earnings).

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.