Is It Worth Considering Dutech Holdings Limited (SGX:CZ4) For Its Upcoming Dividend?

Readers hoping to buy Dutech Holdings Limited (SGX:CZ4) for its dividend will need to make their move shortly, as the stock is about to trade ex-dividend. Investors can purchase shares before the 16th of August in order to be eligible for this dividend, which will be paid on the 29th of August.

Dutech Holdings's next dividend payment will be CN¥0.01 per share, on the back of last year when the company paid a total of CN¥0.049 to shareholders. Based on the last year's worth of payments, Dutech Holdings has a trailing yield of 4.5% on the current stock price of SGD0.22. Dividends are a major contributor to investment returns for long term holders, but only if the dividend continues to be paid. That's why we should always check whether the dividend payments appear sustainable, and if the company is growing.

See our latest analysis for Dutech Holdings

If a company pays out more in dividends than it earned, then the dividend might become unsustainable - hardly an ideal situation. Dutech Holdings paid out a comfortable 37% of its profit last year. Yet cash flow is typically more important than profit for assessing dividend sustainability, so we should always check if the company generated enough cash to afford its dividend. What's good is that dividends were well covered by free cash flow, with the company paying out 22% of its cash flow last year.

It's encouraging to see that the dividend is covered by both profit and cash flow. This generally suggests the dividend is sustainable, as long as earnings don't drop precipitously.

Click here to see how much of its profit Dutech Holdings paid out over the last 12 months.

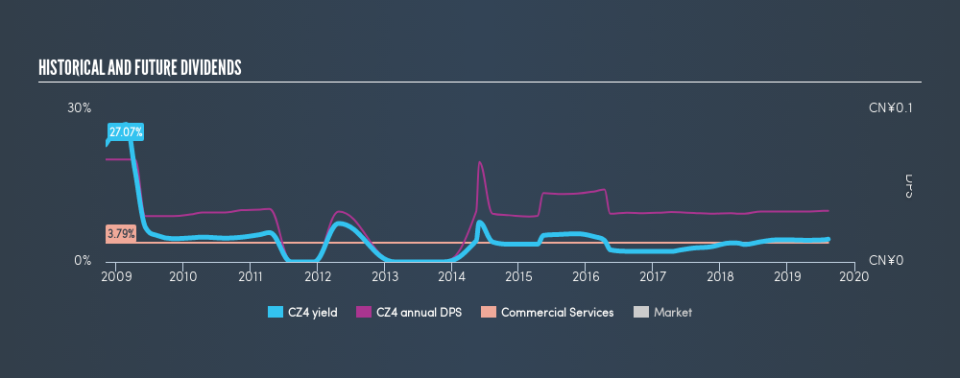

Have Earnings And Dividends Been Growing?

When earnings decline, dividend companies become much harder to analyse and own safely. If earnings decline and the company is forced to cut its dividend, investors could watch the value of their investment go up in smoke. Readers will understand then, why we're concerned to see Dutech Holdings's earnings per share have dropped 13% a year over the past five years. Such a sharp decline casts doubt on the future sustainability of the dividend.

The main way most investors will assess a company's dividend prospects is by checking the historical rate of dividend growth. Dutech Holdings has seen its dividend decline 6.7% per annum on average over the past 10 years, which is not great to see. It's never nice to see earnings and dividends falling, but at least management has cut the dividend rather than potentially risk the company's health in an attempt to maintain it.

The Bottom Line

Is Dutech Holdings an attractive dividend stock, or better left on the shelf? Dutech Holdings has comfortably low cash and profit payout ratios, which may mean the dividend is sustainable even in the face of a sharp decline in earnings per share. Still, we consider declining earnings to be a warning sign. While it does have some good things going for it, we're a bit ambivalent and it would take more to convince us of Dutech Holdings's dividend merits.

Want to learn more about Dutech Holdings? Here's a visualisation of its historical rate of revenue and earnings growth.

A common investment mistake is buying the first interesting stock you see. Here you can find a list of promising dividend stocks with a greater than 2% yield and an upcoming dividend.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.